Anyone involved in the money-transfer business will tell you how difficult it is to obtain access to banking if you are an MSB. MSB Friendly Banks are far and few today, with most of them derisking themselves from the vertical all together. Most incumbent MTOs have lost access to their MSB business account. Whilst others have still managed to hold on to banking relationships, no one knows how long that will last.

Truth be told, the words MSB, Money Transfer Operator, Money Exchange, etc. have become synonymous with the plague.

No one wants it.

No one wants to touch it.

No one wants to speak about it.

Even within the money transfer vertical, there are essentially two different types of companies:

- Person-to-Person (P2P or C2C) money transfers

- Business-to-Business (B2B) money transfers

Understandably, the perceived risk associated with P2P money transfers is higher than B2B transfers. Yet, even for B2B operators, finding access to banking in various markets (for purposes of settlement & disbursement) is difficult.

Today, various operators who are, say, based in UK, UAE, Australia, Hong Kong, US or Canada are finding it almost impossible to get bank accounts opened in other countries to carry out their activities. Something they were able to do, not too long ago, is now an impossible task.

Despite the extensive KYC documentation provided on the corporate entities, and in many cases, clients that are well-known, banks still refuse to provide an MSB business account to these entities. Risk is always cited as the root-cause, without explaining the root cause further.

Frustration Grows

The frustration over the contraction in banking relationships is worrisome for many. In one particular example, a client of mine was processing US$ 200 Million to the US per month. Then the banks pulled the plug.

Imagine the revenue loss.

Today, it has been eight months and the client has not been able to find an MSB friendly bank that would offer them banking services along with SWIFT messaging.

They’ve essentially been locked out from the US economy. US based Dollar clearing is something they cannot execute profitably any longer. They must rely on 3rd party providers to execute their transaction, that too with limits and much reduced profitability.

Another client based out of the UK processes payroll for companies you and I can relate to. Yet, for them to get a bank account opened in Dubai or New York or Sydney has become a major moot point.

Despite the excellent references, elementary visibility into the transaction (from its origination), banks still refuse to provide banking services to such operators. The net loss? This client is now no longer processing payroll activities, which were previously GBP 60 Million a month.

One might question, “Well surely they can go to an FX provider and do business with them?” The answer is the following:

- The operator’s clients deal directly with the FX provider and they see no reason to continue doing business with my client.

- FX providers reach out to the client directly (since they have a direct relationship — a key requirement for taking on business), and

- The margins are reduced. If my client was previously working on a 20 basis points spread, they are lucky to walk away with 5 basis points when working with FX providers who channel their business.

Without hope, many clients have thrown in the towel and others are starting to foster more innovative methods to do transfers.

The Solution

The easiest solution is netting-off transfers with other B2B payment providers. This has huge trust issues, but in this day and age of access-to-banking-vacuum, one really does not have much choice.

The problematic aspect of netting off transfers is to have uniform bilateral flows, which is extremely difficult. Heck, companies like TransferWise started on this premise. But when you go B2B, the flows are anything but bilateral and uniform.

However, MTOs are realizing the potential of bitcoin, which can enable digital movement of value within minutes anywhere in the world.

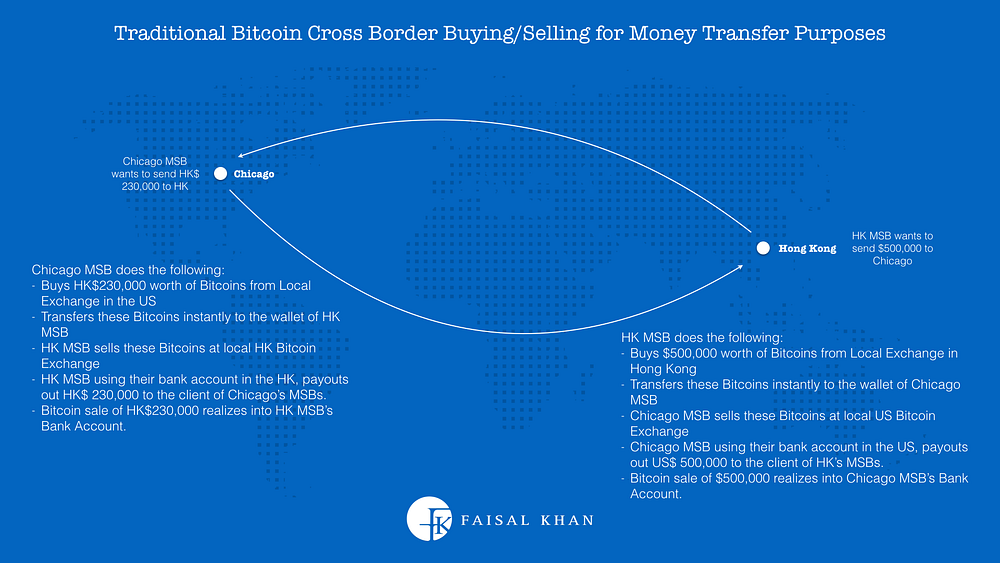

A traditional Bitcoin based Buying/Selling for money transfer purpose would look like this:

While the above diagram may seem very nice, it does have some serious drawbacks.

- Even for very high volume based trades done on Bitcoin exchanges, the minimum fees is 0.1%. For a Buy/Sell trade, this would mean a very minimum of 0.2% (20 basis points) that would be deducted from the price of the transfer.

- Liquidity is an issue. If an MSB in HK wants to suddenly buy US$ 7.3 Million worth of Bitcoins, it could affect the overall buy price. Sometimes, sellers will be short — hence this poses a problem.

- Likewise, after the transfer of Bitcoins, the MSB selling these bitcoins may not have enough buyers on the other end and might have to take a loss on the BTC trade.

- The rates are ever fluctuating on both sides for BTC.

- Not very practical when it comes to doing day-to-day B2B business. The sudden volatility can be costly.

- The B2B market size is between US$ 23 and US$ 28 Trillion a year! (no one knows exactly how big it is).

- US$ 10 Billion market cap of Bitcoin cannot be expected to fulfill even a fraction of the B2B money transfer market.

What Will Eventually Happen

Sooner or later, an alliance of sorts will come about to issue their own digital equivalent of a bitcoin, something that has value tied to the US Dollar and would be accepted and traded between partners.

Either this, or a new coin will emerge, backed by adequate capital that would allow small and medium B2B operators to latch on to it and do transfers worldwide, amongst the members in various different cities.

B2B Transfer coins can be utilized to send value from one country to another. Once the transfers are complete, the coins can be liquidated on various exchanges worldwide. Because the coins would be mapped 1-to-1, say against the US Dollars, operators are assured that there will be no price volatility in buying/selling.

ref : www.faisalkhan.com